When you switch health plans, the biggest surprise isn’t usually the monthly premium. It’s the generic drug coverage - or lack thereof - that hits your wallet. You might think all plans treat generics the same: cheap, simple, and reliable. But that’s not true. A small change in your plan’s formulary can turn a $5 copay into a $40 coinsurance hit. And if you’re on a daily medication like metformin, levothyroxine, or lisinopril, that difference adds up fast - often to over $1,000 a year.

Why Generic Drugs Are Your Best Friend (If You Know How to Use Them)

Generics make up 90% of all prescriptions filled in the U.S., but they only account for 23% of total drug spending. That’s because they work just like brand-name drugs - same active ingredients, same FDA approval - but cost a fraction of the price. When your health plan puts a generic in Tier 1, you pay a flat copay, usually between $3 and $20, regardless of the drug’s actual cost. That’s the sweet spot. But if your drug gets moved to Tier 2 or higher? You could be paying 20-30% of the full price - and that’s before your deductible even kicks in.

Here’s the reality: 68% of people switching plans don’t check if their specific generic formulation is still covered. They assume “metformin” is “metformin.” But if your old plan covered Metformin ER made by Teva, and your new plan only covers the immediate-release version from Mylan, you might suddenly face a higher tier - and a much higher bill.

Tiered Formularies: The Hidden Math Behind Your Prescription Costs

All health plans use tiers to sort drugs by cost. But the structure varies wildly:

- 3-tier plans (common in some employer plans): Generic ($5-$10), Brand ($30-$50), Specialty ($100+)

- 4-tier plans (standard on Healthcare.gov): Tier 1: generics ($3-$20), Tier 2: preferred brands ($40-$60), Tier 3: non-preferred brands ($70-$100), Tier 4: specialty ($150+)

- 5-tier plans (common in Medicare Advantage): Tier 1: preferred generics ($0-$10), Tier 2: non-preferred generics ($20-$40), Tier 3: preferred brands, Tier 4: non-preferred brands, Tier 5: specialty

Medicare Part D plans have their own rules. In 2023, the base deductible was $505 - but many plans waived it for Tier 1 generics. Some even offered $0 copays. Meanwhile, Silver Standardized Plans on the ACA marketplace now waive the entire deductible for Tier 1 generics, meaning you pay just $20 for your monthly meds - even if you haven’t met your medical deductible yet. That’s a game-changer for people on chronic medications.

State Rules Can Make or Break Your Drug Costs

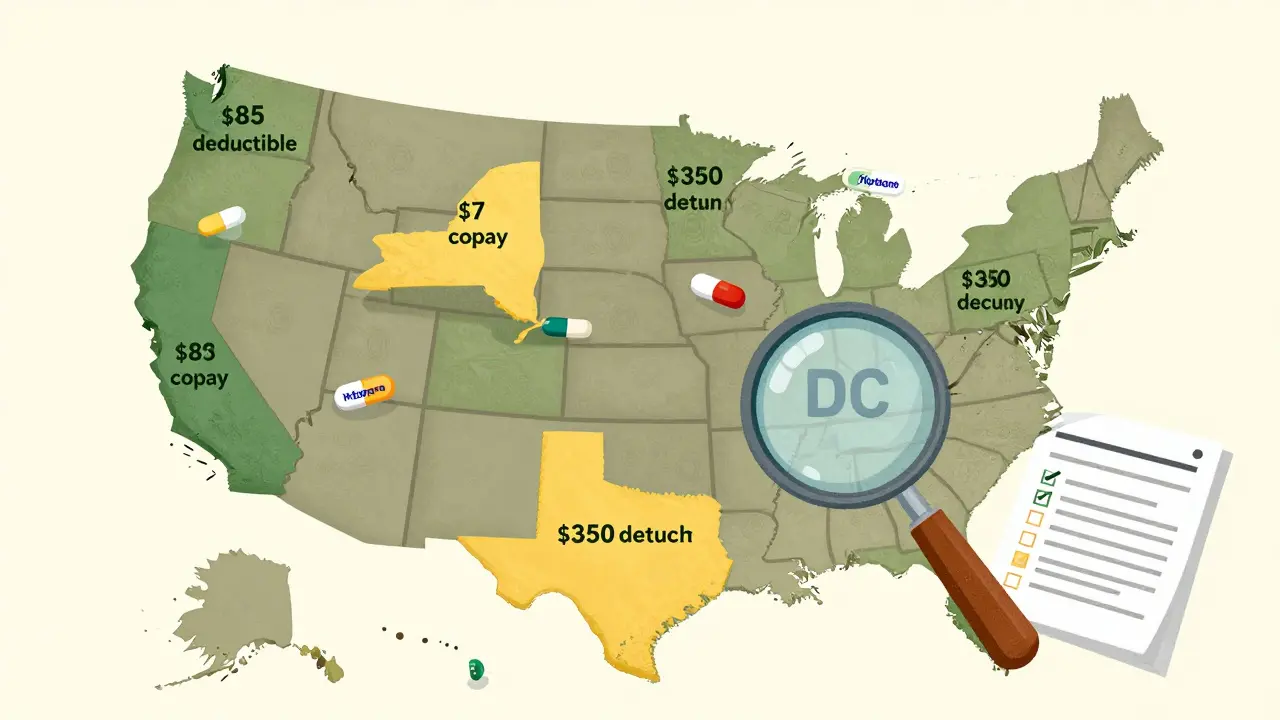

Where you live matters more than you think. California requires a $85 outpatient drug deductible before generics are covered - and then you pay 20% coinsurance up to a $250 cap. New York? No deductible for generics. You pay a flat $7 copay. DC has a $350 separate drug deductible. That means two people on the same exact plan, living 300 miles apart, could pay completely different amounts for the same pill.

And it’s not just about the deductible. Some states mandate $0 copays for insulin, others cap out-of-pocket costs for specialty drugs. If you’re switching plans, you can’t just compare premiums - you need to know your state’s prescription rules.

How High-Deductible Plans Trick You (And How to Avoid It)

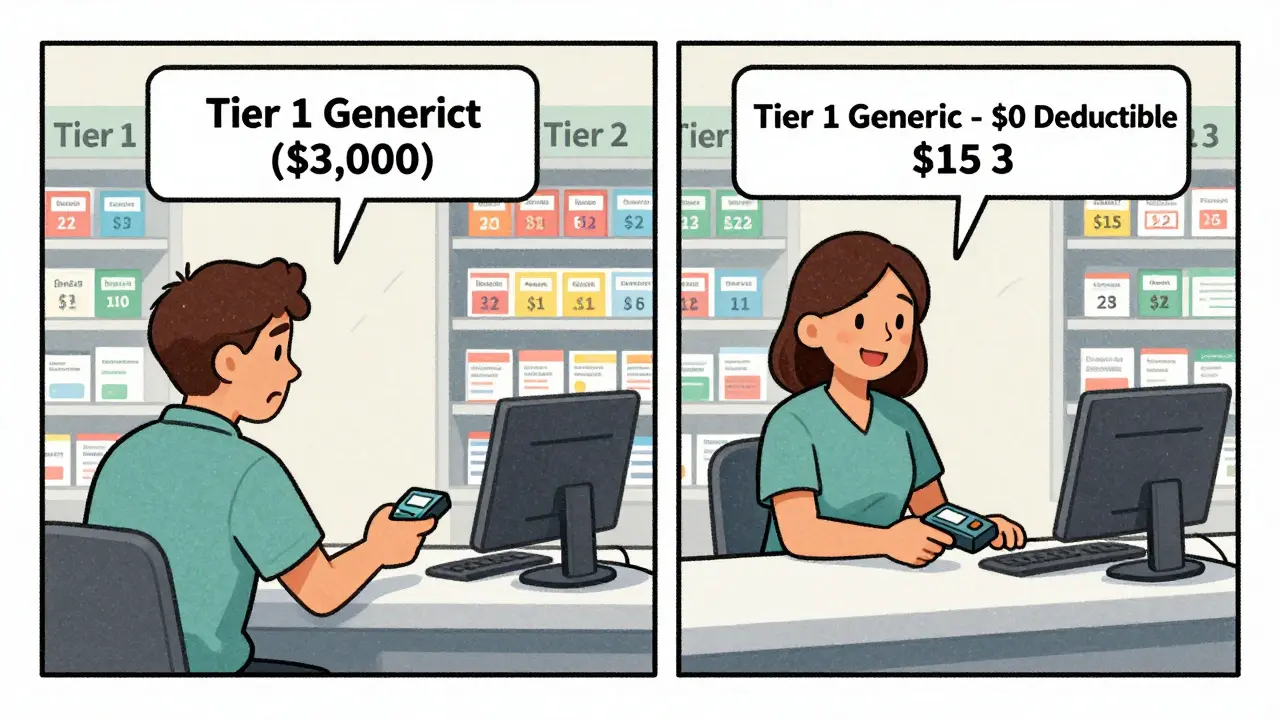

HDHPs look great on paper: low premiums, HSA contributions, tax breaks. But if you take even one daily generic, they can cost you more. Why? Because many HDHPs combine your medical and prescription deductibles. So if your deductible is $3,000, you pay full price for every pill until you hit that number. That’s $1,500 out of pocket just for your blood pressure med before your plan even helps.

Not all HDHPs are like this. Some Silver SPD plans (available in 32 states as of 2024) separate the prescription deductible. That means you pay $20 for your generic, no matter what - even if you haven’t met your $3,000 medical deductible. If you’re on maintenance meds, always look for plans with this structure.

Real-World Cost Differences: A Case Study

Meet Sarah, 58, on three daily generics: metformin (500mg), levothyroxine (50mcg), and lisinopril (10mg). In 2023, she was on a non-standardized plan. Her monthly cost: $120. She paid $40 for each drug - because her plan had a $1,200 prescription deductible, and she hadn’t met it yet.

She switched to a Silver SPD plan in 2024. Now? $3 for metformin, $5 for levothyroxine, $7 for lisinopril. Total monthly: $15. Annual savings: $1,260. And she didn’t even have to meet her $2,500 medical deductible.

That’s not luck. That’s knowing what to look for.

How to Check Your Medications Before You Switch

Don’t guess. Don’t rely on your insurer’s sales rep. Do this:

- Get the full formulary - not just the summary. Look for your exact drug name AND manufacturer. (e.g., “Metformin ER, Teva”)

- Check the tier - Is it Tier 1? Tier 2? If it’s not Tier 1, ask why.

- Verify your pharmacy - Is your local CVS or Walgreens in-network? If not, you might pay 300% more.

- Use the official calculator - Medicare.gov’s Plan Finder or Healthcare.gov’s tool. Enter your drugs, your zip code, your pharmacy. It’ll show you real out-of-pocket costs.

People who do all four steps reduce unexpected drug costs by 73%. That’s not a suggestion - it’s a rule.

What No One Tells You About Generic Formulations

Not all generics are created equal. The FDA says they’re bioequivalent - but some people notice differences. That’s why some doctors prescribe a specific brand of generic. If your plan changes the manufacturer, your body might react. And if that new version isn’t in Tier 1? You’re stuck paying more.

One user on Reddit shared: “My levothyroxine went from $0 to $45 overnight because my plan switched from Teva to Aurobindo. Same drug. Different pill. Different tier.”

Always confirm the manufacturer. Ask your pharmacist: “Is this the same one I’ve been taking?”

The Tools That Actually Work

Not all plan comparison tools are equal. Basic tools on insurer websites are only 78% accurate. But the ones endorsed by CMS - like Medicare Plan Finder and Healthcare.gov’s plan selector - are 96% accurate. They pull data directly from plan filings. Use them. Don’t trust a brochure or a phone rep.

Also, use your pharmacy’s cost estimator. CVS, Walgreens, and Rite Aid all have online tools that show prices at your local store - even for mail-order options. You might save $20 a month just by switching where you pick up your meds.

What’s Coming in 2025 and Beyond

The Inflation Reduction Act capped insulin at $35/month starting in 2023. By 2025, Medicare Part D will cap total out-of-pocket drug costs at $2,000/year. That’s huge. But it won’t fix everything.

By 2026, experts predict generics will split into three tiers: preferred, non-preferred, and “therapeutically equivalent but not preferred.” That means even if two generics do the same thing, one might cost $10 and the other $35. The reason? PBMs are negotiating harder with manufacturers.

And by 2027, most marketplace plans will drop the combined medical-prescription deductible entirely. Why? Because consumers are walking away from plans that hide drug costs. The market is forcing change.

Final Rule: Never Switch Without a Drug Check

Switching health plans is one of the few times you can save money just by doing your homework. You don’t need to be a doctor. You don’t need to be an expert. You just need to spend 30 minutes checking your meds against the new plan’s formulary.

If you’re on one or more daily generics, this isn’t optional. It’s essential. A single misstep can cost you more than your entire premium. And if you’re on Medicare, the stakes are even higher - 15% of beneficiaries lose coverage for their meds during annual enrollment.

Don’t wait until next year. Do it now. Your wallet will thank you.

Sabrina Sanches, March 14, 2026

I switched plans last year and didn't check my generics-big mistake. My levothyroxine went from $0 to $42. I cried in the pharmacy aisle. Now I check every single time. Don't be like me.

Kandace Bennett, March 15, 2026

OMG YES 🙌 I literally wrote a 12-page spreadsheet comparing formularies last year. People don’t realize that "metformin" isn’t one thing-it’s 17 different pills with 17 different price tags. If you’re not checking the manufacturer, you’re basically gambling with your insulin. 💸🩺

Jimmy V, March 17, 2026

You’re all missing the real point. The PBM middlemen are the problem. They force insurers to shuffle generics into higher tiers to squeeze kickbacks from manufacturers. Stop blaming patients. Blame CVS Caremark and Express Scripts. They’re the ones profiting off your confusion.

Rex Regum, March 18, 2026

Oh please. This is just fearmongering. My plan changed my generic from Teva to Mylan and I didn’t even notice. My blood pressure didn’t spike. My thyroid didn’t melt. You’re all acting like switching manufacturers is a betrayal. It’s chemistry. Not a relationship.

Kandace Bennett, March 19, 2026

Rex, you’re the reason people die from uncontrolled diabetes. My mom’s kidney function dropped 30% after they switched her generic without telling her. You think it’s "chemistry"? It’s bioequivalence with side effects. I’ve seen the lab reports. Don’t be that guy.

Kelsey Vonk, March 21, 2026

I love how this thread turned into a public health seminar 🤗 I’m not a doctor but I’ve been on 5 different plans in 7 years. The one thing that never changes? Always check your pharmacy’s price before you enroll. Sometimes the mail-order is cheaper than your local CVS. I save $18/month just by switching. Small wins!

Emma Nicolls, March 21, 2026

i just started taking metformin and honestly i had no idea any of this existed. i thought all generics were the same. now im terrified but also kinda grateful? like wow. this is wild. thanks for the heads up

Richard Harris, March 21, 2026

I’m from the UK and we don’t have this mess. Generics are all £2.99. No tiers. No formularies. No drama. Just pills. I know it’s not the same system but… it’s so simple. I miss it sometimes.

Shruti Chaturvedi, March 23, 2026

Shruti here from India. We have generics too but they cost like $1 a month. No deductibles. No tiers. Just medicine. I know it’s not comparable but I wish we could bring some of that simplicity here. Everyone deserves affordable meds. No matter where you live

douglas martinez, March 24, 2026

The data is clear. Plan formularies are not standardized. The federal government has no oversight on PBM formulary placement. This is a regulatory failure. Consumers must demand transparency. Contact your representative. This isn’t personal-it’s policy.

Emma Deasy, March 26, 2026

The system is a grotesque, labyrinthine nightmare designed by corporate actuaries to extract every last dime from the chronically ill. We have turned healthcare into a game of Russian roulette-where the bullet is a pill with a different manufacturer’s logo. And yet, we are told to be grateful for the "choice". The moral bankruptcy of this system is not merely staggering-it is unforgivable.